Main Syllabus: GS II - Government policies and interventions for development in various sectors and issues arising out of their design and implementation.

Why in the News?

In May 2025, the Supreme Court of India questioned the absence of comprehensive and clear crypto regulation in India.

What is the status of Virtual Digital Assets (VDA) in India?

- Virtual Asset – It is a digital representation of value of assets such as cryptocurrencies, non-fungible tokens (NFTs), gaming tokens, and governance tokens.

A non-fungible token is a unique digital identifier that is recorded on a blockchain and is used to certify ownership and authenticity.To Know More about, NFTs Click Here.

- Grass Root Crypto Adoption - India continues to lead in grassroots crypto adoption, for the second consecutive year in the ‘Geography of Crypto’ report by Chainalysis (2024).

- Retail Investment in VDA - A National Association of Software and Service Companies (NASSCOM) report finds that Indian retail investors poured $6.6 billion into crypto assets.

- Trading Rate - Between December 2023 and October 2024, Indians traded over Rs 2.63 trillion on offshore platforms.

- Employment Potential – NASSCOM report predicts that the industry could create over eight lakh jobs by 2030.

- Strong Developer Base - India also boasts one of the largest and fastest-growing web3 developer cohorts.

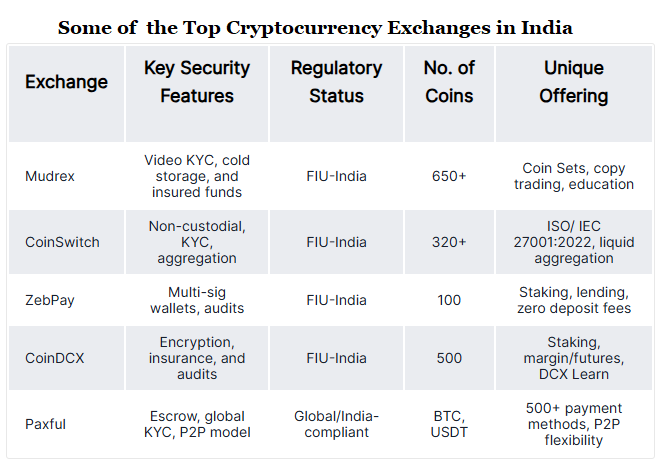

What is the role of Virtual Asset Service Providers (VASP)?

- Virtual Asset Service Provider (VASP) – These are entities that carry out exchanges between different forms of virtual assets or between virtual assets and fiat currencies.

- Examples of Virtual Asset Service Providers – They include cryptocurrency exchanges, ATMs, wallet custodians, and crypto hedge funds.

- Intermediaries - They act as intermediaries, enabling users to engage in actions such as exchanging, transferring, or safekeeping virtual assets.

- Cryptocurrency Exchanges - These organizations facilitate the trading of cryptocurrencies, both for other digital currencies and for fiat money.

- ATMs - Bitcoin ATMs allow customers to buy Bitcoin in exchange for cash, and sometimes to sell it too.

- Wallet Custodians – These organizations administer and store virtual assets, as well as exchange and transfer them.

- Crypto Hedge Funds - Some high-value investors use crypto hedge funds as their investment vehicles.

- Regulation of VDA Industry - These intermediaries facilitate the alignment of the VDA industry with existing laws and enforcement of policies.

What are the current Indian regulations on VDA?

- Definition- The term “Virtual Digital Asset” is defined under Income Tax Act, 1961 and includes cryptocurrencies, non-fungible tokens (NFTs), and any other digital assets notified by the central government.

- Legal Status - Cryptocurrencies and other VDAs are not recognized as legal tender in India.

- This means they cannot be used as official currency for payments, but buying, selling, and holding these assets is legal.

- No Dedicated Regulatory Statue - There is no outright ban on crypto trading or mining, but there is also no dedicated law specifically regulating cryptocurrencies or NFTs as of now.

- Regulatory Oversight - The Reserve Bank of India (RBI), Ministry of Finance, and Securities and Exchange Board of India (SEBI) are the principal authorities overseeing aspects of VDAs.

- AML/CFT Framework – VDA service providers were brought into the ambit of Anti Money Laundering/Counter Financing of Terrorism (AML-CFT) framework under the provisions of the Prevention of Money Laundering Act (PML) Act, 2002 in March 2023.

- The obligation is activity-based and is not contingent on physical presence in India.

- Financial Intelligence Unit-India Registration –VDA SPs operating in India (both offshore and onshore) are required to be registered with FIU IND as Reporting Entity.

What is the taxation regime on VDAs?

- Taxation - The Finance Act, 2022 imposed a flat tax rate of 30% on all income arising from the transfer of VDAs.

- This rate applies to both long-term and short-term gains, with no distinction made between the two.

- No Deductions - The law does not allow any deductions or exemptions other than the cost of acquisition, meaning that expenses such as exchange fees, transaction costs, or mining-related expenses cannot be claimed.

- Denial of Loss Adjustment - Losses from the transfer of VDAs cannot be set off against any other income—whether salary, business profits, or capital gains from other assets.

- Moreover, such losses cannot be carried forward to future years.

- Taxation of Crypto Gift - If a person receives cryptocurrency as a gift, the value of the crypto would be taxed in the hands of the recipient under the head "Income from Other Sources," unless it is received from a relative or falls within other exempt categories.

- GST on Cryptos - Goods and Services Tax (GST) laws may also apply to crypto-related activities, depending on the nature of the transaction.

- Crypto exchanges that provide a platform for buying and selling digital assets are generally considered to be offering a taxable service and are required to pay 18% GST on their commission or platform fees.

- Taxation on Crypto Mining - If mining activity is carried out as a business and crosses the applicable turnover threshold, it may also be treated as a taxable supply of service, attracting 18% GST.

- Payment Taxation - In cases where cryptocurrencies are used as a mode of payment to purchase goods or services, such transactions may be treated as barter and taxed based on the fair market value of the goods or services exchanged.

- When crypto is used to pay for imported services from outside India, such as Web3 development or NFT art, reverse charge GST obligations may arise.

Reverse Charging of GST means the GST will have to be paid directly by the receiver instead of the supplier.

What are the challenges in crypto currency regulation?

- Decentralized Nature of VDAs - India, as a country of strict capital controls and tightly regulated payment systems, has found it difficult to reconcile these frameworks with the decentralised nature of VDAs.

- Ambiguity on VDA - The Reserve Bank of India (RBI), as the domestic regulator of monetary policy, began expressing concerns about the potential threats of crypto as early as 2013.

- In 2018, RBI barred financial institutions from dealing with VDA-related entities which was overturned by the Court.

- Limited Effectiveness of Regulations – Despite restrictive and cautious warning by the government, the VDA market in India saw unassail growth in India.

- Dominance of Non-compliant Platforms - Estimates by various industry reports and think tanks show that between July 2022 and December 2023, Indians traded over Rs. 1.03 trillion worth of VDAs on non-compliant platforms.

- Only 9% of the estimated Rs. 1.12 trillion in VDAs is held on domestic exchanges.

- Limited Success in Banning Platforms - Efforts to block access to non-compliant platforms, such as URL blocking, had limited success.

- Continued Trading in Blocked Platforms - Trade volumes on blocked exchanges rebounded after temporary declines, and web traffic to these platforms rose by 57%.

- Bypassing Restrictions - Users continued to bypass restrictions using virtual private networks (VPN), mirror platforms or servers, and by migrating to other non-compliant exchanges.

- Increasing Crypto Theft - Stolen crypto funds spiked by approximately 21.07% year-over-year (YoY) in 2024 to reach a volume of $2.2 billion.

What lies ahead?

- While the Indian crypto market is yet to be governed by a unified legal code, the introduction of a tax regime and PMLA coverage signifies the government's intent to regulate and not ban.

- Combined with their contributions to national value creation and economic growth, VDA platforms present a more viable and constructive channel for funds to flow through under the oversight of Indian regulators.

- To move beyond the current policy stasis — where tax is levied without meaningful regulation — a balanced, pragmatic and future-proof regulatory framework is necessary.

- Guidelines by global standard-setting bodies, such as the International Monetary Fund, Financial Stability Board, and the Financial Action Task Force, recommends comprehensive and risk-based regulation that is harmonised with international standards.

References

- The Hindu | Regulation Virtual Digital Assets

- Bar and Bench | Crypto Currency Taxation Guide