Staying with the Time-tested NPS System

What is the issue?

The Rajasthan government’s Budget proposal to revert all its employees to the old pension system represents the reversal of a very significant reform.

What is NPS?

- Due to the growing concerns around unsustainable pension liabilities, the government set up an expert committee named Project Old Age and Income Security (OASIS) led by Surendra Dave, to examine policy questions related to old age income security in India.

- This brought together experts and academics, who designed the New Pension System (NPS) in which all new recruits from 1st January 2004 onward were placed into the NPS.

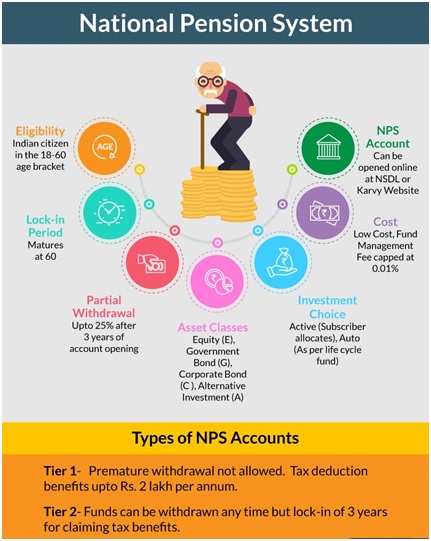

- NPS is a voluntary pension cum investment scheme launched by Government of India to provide old age security.

- It is being administered and regulated by PFRDA set up under PFRDA Act, 2013.

- NPS can be broadly classified into two categories - Government Sector (Central and state governments) and private sector (Corporates and individuals).

- Both resident and Non-resident citizen of India in the age group of 18-65 years including the unorganised sector workers can join NPS, an NRI can also open an NPS account.

- The contribution by governments (both central and state )has been enhanced to 14% to enhance the corpus.

- NPS offers two types of accounts- Tier-I and Tier-II.

- Tier-I account is the pension account having restricted withdrawals.

- Tier-II is a voluntary account which offers liquidity of investments and withdrawals.

- Upon successful enrolment, a Permanent Retirement Account Number (PRAN) is allotted to the subscriber under NPS.

- On retirement or exit from the scheme, the corpus is made available to the subscriber with the mandate that 40% of the corpus must be invested in to annuity to provide a monthly pension post retirement or exit.

What pension schemes were available before 2004?

- Prior to 2004, there were two kinds of pension schemes which were limited in their coverage.

- There was a pension scheme for civil servants and employees of autonomous bodies such as universities, which was fully funded by the government.

- Under the scheme, employees on their retirement used to get usually 50% of their last drawn salary, as pension with dearness relief linked to inflation.

- Also, there is the pension scheme by the Employees Provident Fund Organisation (EPFO), which is mandatory for establishments covered by the EPFO (companies with more than 20 workers).

- Employee Pension Scheme (EPS) works only if assured returns are replaced by market determined rates of return.

- However since there are strict norms on governing portfolio management, higher returns cannot be obtained by better fund management.

The EPFO is a social security organisation which functions under the Employees' Provident Funds Act, 1952 to extend universal coverage and ensure Nirbadh (seamless and uninterrupted) service delivery to its stakeholders.

What is the significance of NPS?

India is expected to see a 41% spike in its elderly population in the next decade with its old age dependency ratio likely to rise from 15.7% to 20%.

- The market-linked NPS is superior to the defined-benefit system both from a fiscal and welfare standpoint.

- The NPS’s objective was to move away from concentrating the government’s pension obligations from a thin slice of the population to the wider population and to the poor and unorganised workers.

- The NPS requires both the employer and the employee to make regular contributions during the employee’s working life, which gets invested in market instruments to build a corpus that can be used to fund pensions after 60.

What are the implications of reverting back to old pension system?

- Fiscal implications- The reversion to the old pension system will have fiscal implications as the government would either have to cut on investments or borrow more to pay for a higher pension bill under the old pension system.

- Hamper developmental expenditure- It would also burden future generations with increasing pension payouts that crowd out developmental expenditure.

- Affects pan India pension system- By going back to giving a defined benefit pension to civil servants, the Rajasthan government will reduce the chances of creation of a nationwide pension system for all workers.

- Inequity- The proposal will reintroduce inequity into old age benefits of the Indian population.

What is the way forward?

- It must be recognised that there are short-term fiscal pressures that propel State governments to kick the can down the road.

- Presently, with both the old and new pension systems in operation, States are dealing with the twin burden of funding pensions for their retirees, along with NPS contributions.

- The Centre and the Finance Commission can perhaps offer States some fiscal leeway to address this anomaly.

- The government, with PFRDA, can also do more to showcase NPS’ advantages to employees, while addressing their genuine concerns.

- Employees who would like to avoid stock market volatility can choose to invest only in the corporate bond or government securities options in the NPS.

- To address subscriber concerns about uncertain pension payouts, the Centre needs to do away with the restrictive rules governing the end-use of the accumulated NPS corpus.

- The annuity schemes on the NPS menu need to be improved with better returns and tax breaks on annuity income.

PFRDA, the authority established through the PFRDA Act, 2013 is ensuring the orderly growth and development of pension market.

References

- https://www.thehindubusinessline.com/opinion/editorial/future-imperfect/article65202022.ece

- https://www.pfrda.org.in/index1.cshtml?lsid=1757

- https://npscra.nsdl.co.in/all-faq-about-nps.php

- https://theprint.in/ilanomics/rajasthans-pension-system-reversal-is-anti-reform-it-will-reintroduce-inequality/858633/