Why in News?

Latest data from the Reserve Bank of India (RBI) showed that deposits grew at a lower rate than the bank credit growth rate signifying higher loan-deposit ratio.

What is loan-deposit ratio?

- Recent findings – RBI data shows that Indian banking system has a high loan–deposit (LD) ratio of about 77.2%.

- LDR – It is the ratio of the total amount of loans given out by the bank to the total amount of deposits held by the bank.

Deposits refers to which the customers keep with the bank and get interest for. Credit refers to which the bank lends to customers at an interest rate charged from them.

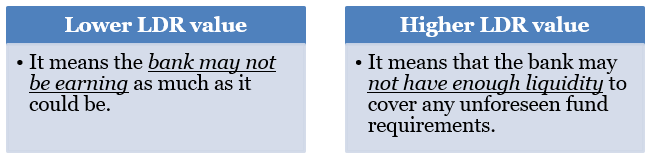

- Role – It is used to assess a bank's liquidity by comparing a bank's total loans to its total deposits for the same period.

- It also helps to ensure that banks are not overexposed to risk.

- Determining factors - There are several factors like the economy, interest rates, and the bank's lending policies.

- For example, during an economic recession, banks may become more risk-averse and tighten their lending policies, resulting in a lower LDR.

- Measurement - It is measured and expressed as a percentage.

- Impact of high LDR – As the gap increases between deposits and credit, it creates an asset-liability mismatch for lenders.

- It may potentially expose the system to structural liquidity issues.

What is the role of capital market in reducing bank deposits?

- Outflow of household savings from banks – Households and consumers who traditionally leaned on banks for parking or investing their savings are increasingly turning to capital markets and other financial intermediaries.

- Over the last year or so, Indian households have increasingly channelled their savings to capital markets.

While bank deposits continue to remain dominant as a percentage of financial assets owned by households, their share has been declining with households increasingly allocating their savings to mutual funds, insurance funds and pension funds.

- Surge of capital markets – After the Covid-19 pandemic, the Indian capital markets have seen a surge in retail activity through direct (direct trading) and indirect (using mutual fund route) channels.

- Economic Survey 2023-24 - The number of demat accounts with rose from 11.45 crore in FY23 to 15.14 crore in FY24 with respect to both depositories NSDL & CDSL.

National Securities Depository Ltd (NSDL) is an Indian central securities depository, based in Mumbai. It was established in August 1996 as the first electronic securities depository in India.

Central Depository Services Ltd (CDSL) is the second Indian central securities depository based in Mumbai. It is the largest depository in India in terms of number of demat accounts opened.

- Rise in retail participation – It was more substantial and steadier through the indirect channel via mutual funds.

- The net AuM (assets under management) of the mutual fund industry grew by 6.23% as of July 2024.

- The mutual funds segment presently has about 9.33 crore systematic investment plan (SIP) accounts through which investors regularly invest in schemes.

- Easier investment process – Higher returns and robust digital infrastructure which has eased the investment process

- Rapid smartphone penetration – It have facilitated the entry of more retail investors into capital markets.

What are the measures taken?

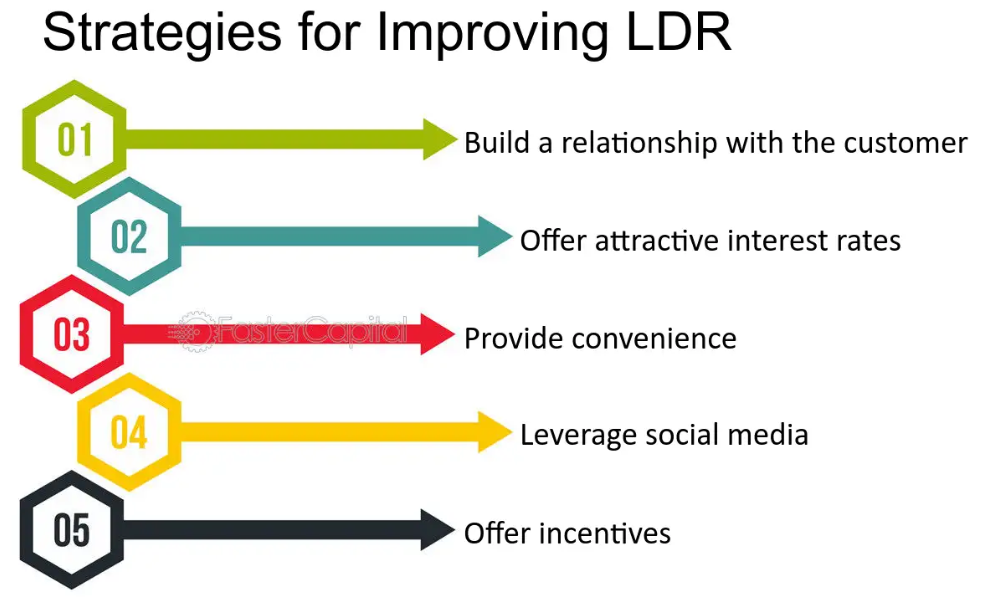

- Guidelines – The government and the RBI have asked lenders to focus more on deposit mobilisation through innovative products.

- They urged banks to garner more deposits by leveraging their wide branch network and offering innovative products.

- Special retail deposit schemes – It was launched by lenders such as State Bank of India, Bank of Baroda, Bank of India, Bank of Maharashtra, RBL Bank and Bandhan Banks.

- Amrit Vrishti - It was launched by SBI, a scheme that offers 7.25% interest on deposits for 444 days.

- Monsoon Dhamaka – It was launched by Bank of Baroda, a deposit scheme, offering interest rates of 7.25% for 399 days and 7.15% for 333 days.

What lies ahead?

- Banks can offer higher interest rates on deposits, launch promotional campaigns, and providing excellent customer service.

- Banks need to take the old-fashioned route to bring back focus on mobilising small deposits and not just big deposits to reverse the flagging deposit growth rate.

- Policymakers can also attempt to encourage savers to shift their investments from other asset classes to bank deposits.

References

- The Indian Express| Reason for Slower Bank Deposit Growth

- Investopedia| Loan Deposit Ratio (LDR)