Why in news?

The Reserve Bank of India (RBI) has ordered a certain card network to stop “unauthorised payments” made using business cards.

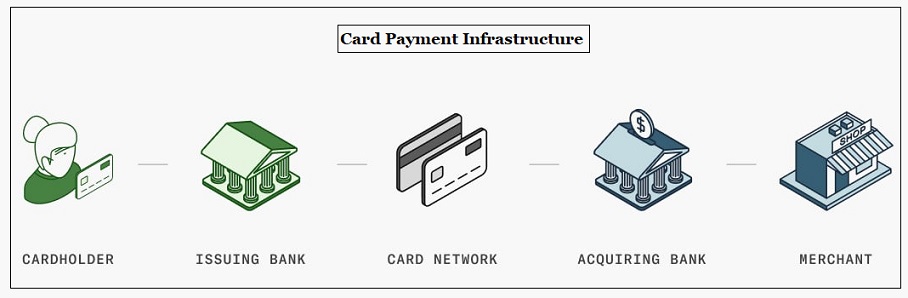

|

Card network |

|

What is the issue?

The Master Direction on KYC is a set of guidelines issued by the RBI to ensure that the entities regulated by it follow certain customer identification procedures and monitor their transactions to prevent money laundering and terrorist financing

|

Key provisions of Payment and Settlement System Act, 2007 |

|

|

Key aspect |

Description |

|

About |

It provides for the regulation and supervision of payment systems in India and designates the Reserve Bank of India as the authority for that purpose and all related matters. |

|

Definition of payment system |

It is a system which enables a payment between a payer and a beneficiary, including clearing, payment, or settlement service, but it does not include a stock exchange. |

|

Designation of payment system |

The Act empowers the Reserve Bank of India (RBI) to designate payment systems in India |

|

Regulation |

The RBI has the authority to regulate and oversee payment and settlement systems to ensure their efficiency, integrity, and stability. |

|

Consumer protection |

The Act outlines the rights and responsibilities of consumers and the obligations of payment system providers to ensure consumer protection. |

|

Offences |

It includes unauthorized operation of a payment system, failure to comply with the terms of authorization, failure to produce statements, return information, or documents providing false information, disclosure of prohibited information, violating the provisions of the Act, not acting in compliance of the directions given by the RBI. |

|

Penalty |

RBI is empowered to initiate a criminal proceeding against the offender. RBI can even impose fines on the person for contravening certain provisions of the Act. |

Quick facts

|

Immediate Mobile Payment Services (IMPS) |

|

|

RTGS (Real Time Gross Settlement) |

|

|

NEFT (National Electronic Fund Transfer) |

|

References