Why in news?

The Reserve Bank of India (RBI) has launched a crackdown on some P2P lending platforms for regulatory breaches, including Ponzi-like schemes, illegal deposit-taking, and aggressive recovery methods.

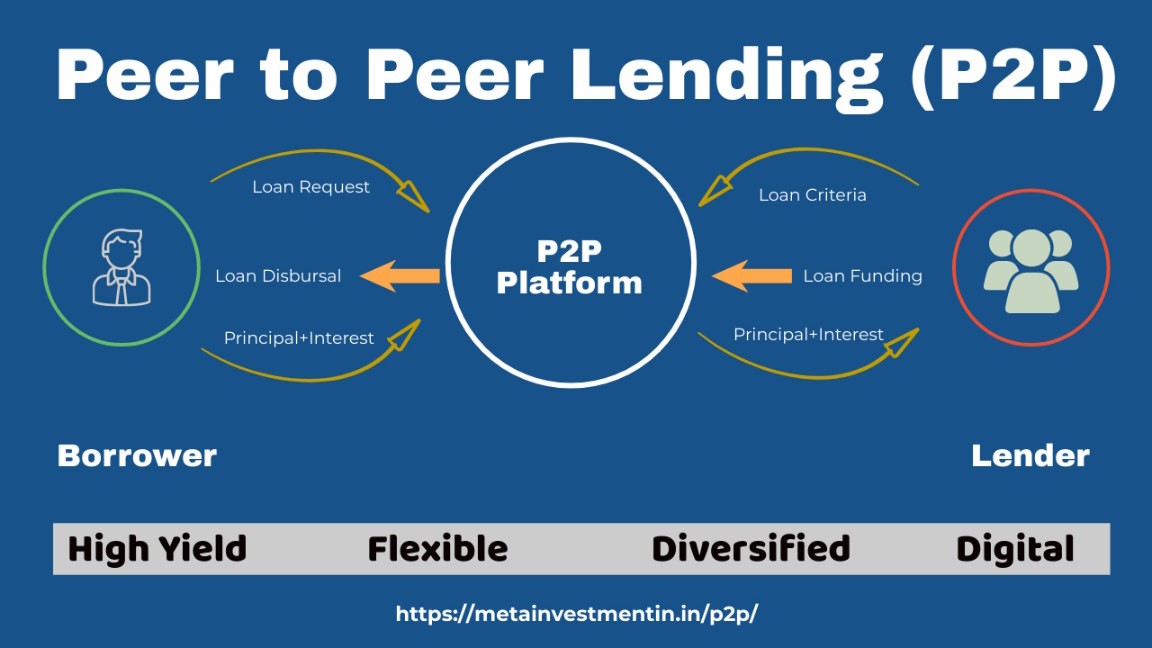

What is NBFC-P2P lending platforms?

- NBFC-P2P- It is the Non-Banking Financial Company - Peer-to-Peer lending platforms are financial intermediaries.

- Role – It enables direct borrowing and lending between individuals, bypassing traditional financial institutions.

- It offers accessible credit to underserved groups and attractive investment options for lenders.

- Tech-Driven credit solutions- They use technology to assess the creditworthiness of borrowers, match them with suitable lenders, and facilitate loan transactions.

|

Regulation in India

|

- It is regulated by the Reserve Bank of India (RBI).

- Mandate registration- Only NBFCs can register as P2P lenders with permission and must obtain a certificate of registration.

- Capital limit- The RBI sets a minimum capital requirement of Rs. 2 crores to set up a P2P platform.

|

What are the concerns highlighted by RBI?

- Breaching of regulations – They significantly have high balances in escrow accounts.

An escrow account is a bank account that holds money or assets until certain conditions are met by the parties involved in a transaction.

- There has been high non-performing asset (NPA) levels.

A NPA is a loan or advance for which the principal or interest payment remained overdue for a period of 90 days.

- Delayed disbursement - Funds transferred by lenders not being immediately disbursed to borrowers, kept in escrow accounts for long periods while assured returns were provided.

- Non-compliance- There is a violation in net owned fund and disclosure requirements.

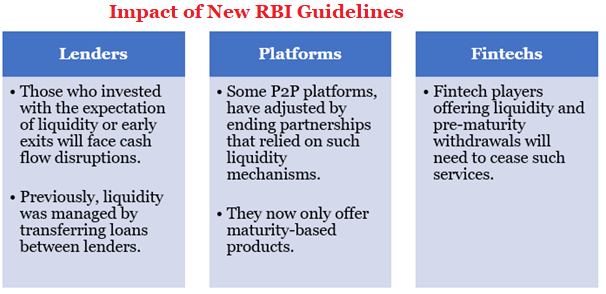

- Operating models allowing premature recall of funds by lenders, which were replaced by new lenders without transparency.

- Profit Margins and High Interest- No cap on interest charged to borrowers, leading to exorbitantly high rates.

- Platforms profiting from the spread between the returns paid to lenders and the interest charged to borrowers.

- Capital diversion- Risk of capital diversion from banks and similar financial institutions due to the appeal of high assured interest rates and immediate liquidity options.

What are the new guidelines by RBI?

- Deposit controls – They are prohibited from accepting public deposits, lending directly, or arranging guarantees for lenders.

- Loan Disbursement Rules- Loans should not be disbursed unless lenders and borrowers are matched according to a board-approved policy.

- Transactions between lenders are now prohibited.

- Monitoring transactions - All fund transfers between lenders and borrowers must be conducted through escrow accounts.

- Funds in escrow accounts must not remain there for more than one day beyond the date of receipt (T+1 rule).

- Prohibition on early withdrawals- They can no longer offer early withdrawals or liquidity options that allowed lenders to exit before the maturity of loans.

- Disclosure of losses- The RBI mandates full disclosure of any losses incurred by lenders on principal or interest which aims to enhance transparency and risk awareness.

- No investment product promotion- They must not promote peer-to-peer lending as an investment product offering features like assured minimum returns or liquidity options.

- Prohibition on Cross-Selling- NBFC-P2P platforms are prohibited from cross-selling insurance products that act as credit enhancement or credit guarantees.

What lies ahead?

- A robust regulatory framework is essential to ensure the stability and credibility of the P2P lending market.

- Refining guidelines to safeguard both borrowers and lenders.

- Educating potential borrowers and lenders about the P2P lending model, its benefits, and its risks is crucial.

- Building and maintaining trust is crucial for the success of P2P lending platforms.

- Adopting best practices and leverage new age technologies to overcome challenges and achieve sustainable growth.

References

- Business Standard| Issues with P2P Lenders

- Business Standard | New Norms for P2P lending platforms

- Business Today| Impact of new Rules on P2P Lenders