Why in news?

Union tax revenue among States is distributed by the Finance Commission based on equity and efficiency principles.

What is the issue?

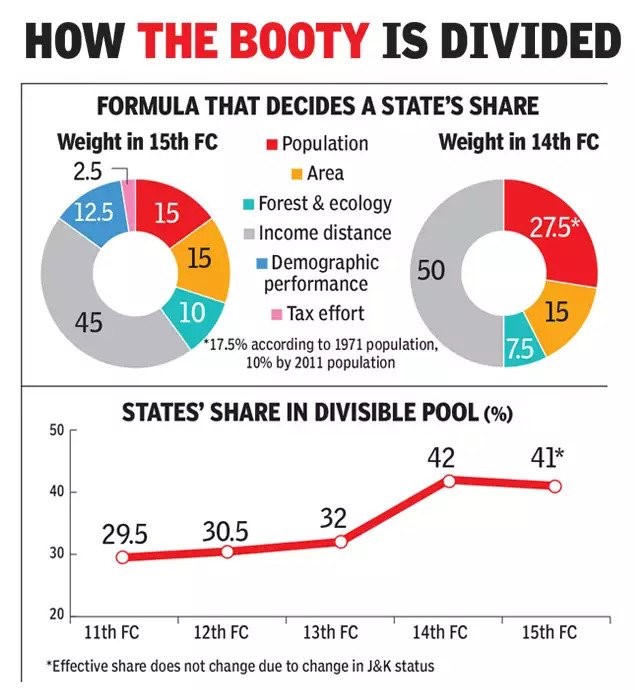

- The Finance Commission recommends a distribution formula specifying each State’s share in the part of the Union tax revenue assigned to States.

- Such distribution formulas have a few weighted determinants.

- Some States have been arguing that their contribution to the Union tax revenue have been higher and, therefore, they rightfully have higher shares in the Union tax revenue.

- In the first eight Finance Commissions, tax contribution with very little weight was a determinant in the distribution formula.

- Since the 10th Finance Commission, this tax contribution was dropped from the distribution formula.

The Finance Commission is a constitutional body that was established under Article 280 of the Indian Constitution.

Why tax contribution is not a good indicator?

- Income origin- A person may pay income tax from one State though the income earning is from other States.

- Low weightage- Successive Finance Commissions have assigned 10% to 20% weight to income tax revenue collection/assessment in the distribution formula for income tax revenue because collection is not a good indicator of contribution.

- Lack of data- Due to the unavailability of proper consumption statistics, contribution was never a determinant in the distribution formula for Union excise duties.

What is the role of Finance Commission in tax revenue transfers?

- State share in Union tax revenue- Finance Commission devises a distribution formula based on the principles of equity and efficiency.

- Equity- The revenue-scarce States and States with higher expenditures get larger shares of Union tax revenue than others.

- Efficiency- Reward the States that are efficient in collecting revenue and rationalising spending.

- Tax contribution- It is an efficiency indicator because a State’s level of development and economic structure decides its tax contribution.

- Population- It is a chief indicator of the expenditure needs of the State, was given 80% to 90% weight in the first seven Finance Commissions as far as income tax distribution was concerned.

- Union Excise duties- The entire distribution was based on population or other indicators of expenditure needs such as area, per capita income etc.,

Since the 10th Finance Commission, the Commission has recommended a single distribution formula for both income tax and Union excise duties. Thus, the Finance Commissions have always favoured assigning more than 75% weight to equity indicators.

- Pooled Central tax- It included tax effort and fiscal discipline as efficiency indicators with a weight of 15%.

- Tax effort-It is broadly defined as the ratio of own revenue of a State to its Gross Domestic Product.

- Fiscal discipline- It is the proportion of own revenue to the revenue expenditure of a State.

To know about the report of 15th Finance Commission, click here

How the tax contribution can be included in the distribution formula?

- GST - It is a consumption-based destination tax which is a good measure of tax contribution and efficiency of States.

- GST is a unified tax system which reflects the accurate tax base of each State and is not affected by discretionary policies.

- Petroleum consumption- It is another measure of tax contribution and efficiency, as it captures the relative share of Union excise and customs duties on petroleum products paid by each State.

- Both the GST and petroleum consumption indicate the relative differences in the incomes of the residents of each State, as consumption is a function of income.

- Recommendation to 16th Finance Commission- As both indicators account for large share of States’ share in the Central tax revenue, they can be included in the distribution formula with a weightage of at least 33%.

Reference

The Hindu- Revisit tax contribution by States