Mains: GS II – Constitutional Bodies

Why in News?

Recently there has been a growing concerns among the states regarding the devolutions of the finance commission.

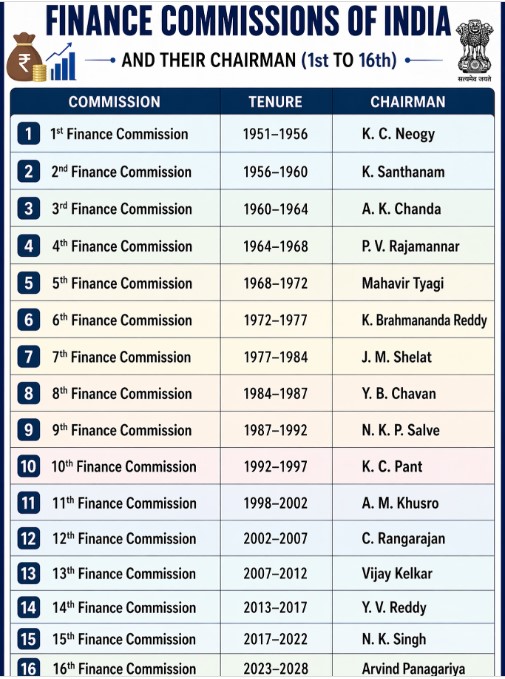

What is Finance Commission?

- The Finance Commission (FC) – The Finance Commission of India is a constitutional body established by the President under Article 280 of the Constitution.

- Key Functions – The Commission is designed to ensure fair fiscal federalism and address the gap between the revenue powers and expenditure responsibilities of the Centre and the States.

- Tax Distribution – Recommending the share of net proceeds of taxes to be divided between the Centre and the States, and allocating those shares among the States themselves.

- Grants-in-Aid – Formulating principles governing the grants-in-aid of the revenues of the States out of the Consolidated Fund of India.

- Local Finances – Recommending measures needed to augment the Consolidated Fund of a State to supplement the resources of Panchayats and Municipalities based on the recommendations made by the State Finance Commissions.

- Other Matters – Making recommendations on any other matter referred to it by the President in the interest of sound finance.

What are the Structure & Composition of FC?

- Appointment – Constituted every fifth year (or earlier if deemed necessary by the President).

- Structure – Consists of a Chairman and 4 other members appointed by the President.

- The Chairman – The Chairman must be a person with extensive experience in public affairs.

- Qualification – The qualifications for members of the Finance Commission of India are determined by the Parliament through the Finance Commission (Miscellaneous Provisions) Act, 1951.

- The four other members are selected from individuals who meet at least one of the following criteria:

- Judicial – They are, have been, or are qualified to be appointed as a Judge of a High Court.

- Accounts & Finance – They have specialized knowledge of the finances and accounts of the Government.

- Administration – They possess wide experience in financial matters and administration.

- Economics – They possess special knowledge of economics.

- Disqualifications – Under the same 1951 Act, a person is disqualified from being appointed or continuing as a member if they:

- Are of unsound mind.

- Are an undischarged insolvent.

- Have been convicted of an offense involving moral turpitude.

- Hold any financial or other interest that is likely to prejudicially affect their functions as a member.

What are the recommendations and criteria of the 16th finance commission?

- Vertical devolution – The 16th Finance Commission retained the 41% vertical devolution share.

- Cess & Surchrges – The FC accepted the Centre’s argument that cesses and surcharges should remain outside the divisible pool because they finance welfare and infrastructure programmes benefiting States indirectly.

- Abolition of certain grants – The Commission also abolished revenue-deficit grants as well as sector-specific and State-specific grants.

- Restrictions on borrowing power of states – It recommended that States should discontinue off-budget borrowings, bring all liabilities onto their budgets, and maintain fiscal deficits below 3% of Gross State Domestic Product (GSDP).

- Horizontal devolution – The Commission used six criteria for horizontal devolution:

- Income distance – 42.5%

- Population – 17.5%

- Area – 10%

- Forest cover – 10%

- Demographic performance – 10%

- Contribution to national GDP – 10%

What are the concerns raised on vertical devolution?

- The GDP criterion – Instead of using actual GSDP shares, the Commission adopted a square-root transformation formula.

- This reduced the relative advantage of economically stronger States such as Maharashtra, Tamil Nadu, and Karnataka while increasing the shares of smaller States.

- Increase of vertical share – Several States demanded that the vertical share should be increased to 50% because their fiscal pressures have increased substantially in recent years.

- Cess & surcharges – One major concern relates to the growing share of cesses and surcharges in the Union government’s tax revenues.

- Since these revenues are not included in the divisible pool, States do not receive any share from them.

- The share of cesses and surcharges has crossed 15% of gross tax revenues, thereby reducing the effective transfers to States.

- Consequently, States demanded either their inclusion in the divisible pool or a cap of around 8% to 10%.

- Non tax revenue – States also argued that the Centre enjoys substantial non-tax revenues from sources such as natural resource extraction, asset monetisation, and surplus transfers from the Reserve Bank of India.

- These revenues further strengthen the Centre’s fiscal position while the States continue to face increasing expenditure responsibilities.

- Mounting fiscal pressures on states – The fiscal position of States has deteriorated due to multiple factors.

- The COVID-19 pandemic increased public expenditure while simultaneously reducing revenue collections.

- GST reforms – In addition, structural changes introduced under the Goods and Services Tax (GST) regime reduced the taxation autonomy of States.

- The recent rationalisation of GST rates from four slabs to two principal rates has further constrained revenue flexibility.

- Growing dominance of Centrally Sponsored Schemes (CSS) – These schemes increasingly require States to contribute a larger share of expenditure.

- For example, under the revised framework of the National Rural Employment Guarantee programme, States are required to bear 40% of programme costs.

- Such arrangements reduce the fiscal autonomy of States because expenditure priorities are increasingly determined by the Centre.

- Slowdown in the buoyancy of central taxes – It has reduced the pace of revenue growth available for devolution.

- As a result, States fear that their fiscal space will continue to shrink in the coming years.

What are the debate over horizontal devolution?

- Arguments of economically stronger states – Traditionally, Finance Commissions have emphasised equity by allocating larger shares to poorer and fiscally weaker States.

- The 16th Finance Commission continued this approach by assigning the highest weight of 42.5% to the income-distance criterion.

- However, economically stronger States have criticised this method because they believe it excessively rewards poorer States while penalising States that have performed better in economic growth, fiscal discipline, and population control.

- Over time, the share of major beneficiary States such as Uttar Pradesh, Bihar, Madhya Pradesh, and West Bengal has increased significantly.

- Their combined share rose from 42.5% during the Sixth Finance Commission period to nearly 51% under the 15th Finance Commission.

- In contrast, the combined share of southern States such as Andhra Pradesh, Karnataka, Kerala, and Tamil Nadu declined from 24.8% to 15.8%.

- This trend has intensified concerns among southern States that they are being penalised for successful governance and economic performance.

- Limited Impact of Fiscal Transfers on Development – Despite increasing transfers to poorer States, regional disparities in public service delivery continue to persist.

- Large differences remain in health and education expenditure across States.

- For instance, Bihar spent only Rs.937 per person on health in 2022-23, while Arunachal Pradesh spent Rs.10,148 per person.

- Similarly, Bihar’s per-student expenditure on elementary education was far lower than that of States such as Sikkim.

- These examples suggest that unconditional fiscal transfers alone may not ensure convergence in development outcomes.

- Critics argue that excessive equalisation transfers can weaken incentives for revenue mobilisation, governance reforms, and fiscal discipline in poorer States.

- Alternative Devolution Scenarios – The alternative weighting schemes could have produced significantly different outcomes.

- If GDP contribution had received a 25% weight instead of 10%, and the weight assigned to income distance had been reduced, economically stronger States would have received substantially larger transfers.

- For example, Maharashtra, Karnataka, and Tamil Nadu would have gained additional transfers amounting to lakhs of crores over the award period.

- Given that the total vertical transfers during the Commission’s award period are estimated at Rs.104 lakh crore, even small percentage changes in devolution shares have enormous fiscal implications.

- This debate reflects the broader tension between equity and efficiency in India’s fiscal federal structure.

- The Political Economy Dimension – The issue also has an important political dimension.

- In India, unlike federations such as Australia or China, economically stronger States are not necessarily the most politically influential in terms of parliamentary representation.

- Consequently, States with larger populations often receive greater fiscal transfers despite weaker economic performance.

- The issue may intensify further after delimitation because northern States are expected to gain greater representation in Parliament.

- This could strengthen political incentives for larger fiscal transfers toward populous States.

What lies ahead?

- The recommendations of the 16th Finance Commission reveal the continuing challenge of balancing equity and efficiency in Indian fiscal federalism.

- While poorer States require greater support to overcome developmental disadvantages, economically stronger States seek recognition for their contribution to national growth, fiscal discipline, and demographic management.

- Future Finance Commissions must therefore adopt a more balanced and data-driven approach.

- Greater emphasis should be placed on fiscal capacity, tax effort, governance quality, and developmental outcomes rather than relying predominantly on non-fiscal indicators.

- Mechanisms such as principal component analysis can help create a more objective and transparent framework for assigning weights.

- Ultimately, a sustainable fiscal federal system must combine equity with incentives for efficiency so that all States remain motivated to contribute to India’s long-term economic development.

Reference

The Hindu| FC & Devolution Issues