Why in news?

Recently, some fintech companies showed interests to join the India’s central bank’s digital currency project.

What is E-Rupee / Central Bank Digital Currency?

- It is a digital currency issued by the RBI.

- Need – It was thought of as an alternative to cryptocurrencies which progressively lose their value.

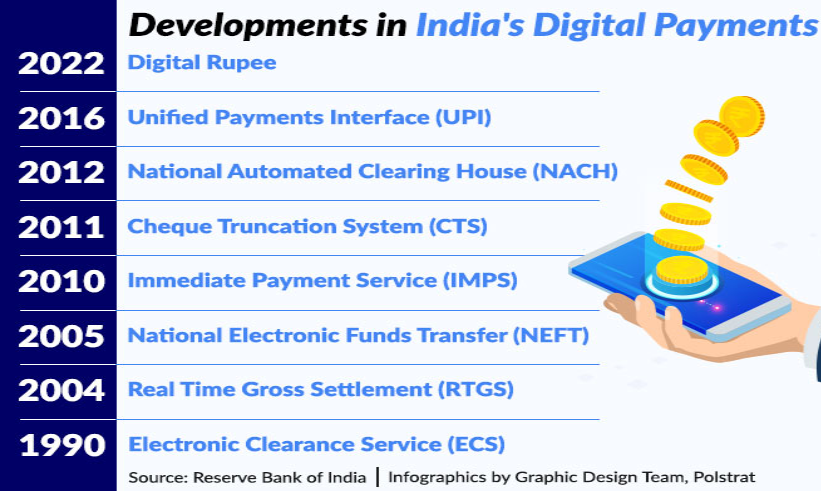

- Launch - It was launched on a pilot basis in 2022.

- Aim - It is aimed at creating an additional option for using money.

- Types – CBDC Retail and CBDC Wholesale.

- Features – It is available entirely in electronic form and does not leave a computer network.

- It is a legal tender like banknotes that can be used for making transactions.

- It could be used for both person-to-person and person-to-merchant transactions.

- Different from bank deposits – Unlike bank deposits, digital rupee in users’ wallets does not attract interest payments from bank.

- Deposits held in banks can be converted into digital rupees and vice versa for ease of use.

- Importance – It would bring greater transparency to transactions and lower the costs associated with the production of traditional fiat currencies.

To know more about CBDC, click here

What are the trends of e-rupee in India?

- Initial uptake – At the time of launch, witnessed growing adoption, with transactions using the digital currency rising to over 1 million a day late last year.

- Gradual decline - since the initial uptake, its use has declined sharply to about 100,000-200,000 a day.

- Reasons for decline - RBI has stopped offering incentives to users and banks that participated in the pilot.

- Limited features and user base compared to a full-scale launch restrict widespread adoption.

- CBDC transaction is not enabled in UPI, which is the most popular digital transaction method.

- Future prospects - RBI is planning to enable the CBDC transactions offline without the need of internet and plans to introduce programmability in CBDC retail payments

|

Benefits of Programmability of CBDC

|

- It enables the CBDC to be used for specified purposes.

- It will permit users like, for instance, government agencies, to ensure that payments are made for defined benefits.

- Corporates will be able to programme specified expenditures like business travel for their employees

- Validity period or geographical areas within which CBDC may be used can also be programmed.

|

Why are fintech companies joining the e-rupee project?

- Initially, the RBI allowed only banks to offer e-rupee via their mobile apps but recently it has announced that payment firms could also offer e-rupee transactions once approved.

- Need of RBI – It has been looking to increase the adoption base for the digital rupee, and rollout on popular fintech platforms could be the push it needs.

Fintech companies are the companies that offer financial services or applications that rely heavily on technology. They use technology to change how consumers interact with the financial industry.

- Fintech’s interest in e-rupee – Fintech companies like PhonePe, Amazon Pay, Cred, and Mobikwik are looking to join by allowing their users to transact in e-rupee via Unified Payments Interface (UPI).

Fintech companies such as GooglePay, PhonePe, Amazon Pay, MobiKwik, and Cred currently account for over 85% of digital payments via UPI.

- Impact of Fintech in CBDC - It will enables payment transactions between users beyond the registered banks in the country.

- It incentivizes private research on central bank digital currency.

- It opens up new platform for startups to rise in financial services sector and can facilitate the invention of new financial products such as insurances, credit services to suit specific needs.

- It enables the Indian fintech companies to provide international services.

- It enhances financial inclusion by making financial services more accessible and promotes the digital economy of the country.

What lies ahead?

- Launch the full-scale version of the digital currency as it is still in pilot basis.

- Include more stake holders and users in the CBDC ecosystem.

- Find more use cases for e–Rupee across the sectors.

- Release the additional features such as off line use, programmability.

- Allow offline capability to enable these transactions in areas with poor or limited Internet connectivity.

- Educate users about using CBDC and its benefits.

- Promote further research on digital currency ecosystem with upcoming technologies.

- Provide incentives to people and companies increase the adoption of e-Rupee.

References

- The Hindu | CBDC Fintech companies

- The Hindu Business Line | Future prospects for CBDC