Mains: GS – III – Economy

Why in News?

UPI, now 10 years old, has become India’s backbone for digital payments, has not just transformed payments in India, but the behaviour of customers and merchants.

What is UPI & it’s working?

- UPI (Unified Payments Interface) – It is India’s mobile-based, real-time payment system that allows instant money transfers between bank accounts using a smartphone app, without needing to enter sensitive bank details each time.

- Purpose – To simplifies digital payments by linking multiple bank accounts to one app.

- Developed by – NPCI on 2016, which has transformed digital payments ecosystems.

- Regulated by – Reserve Bank of India (RBI).

- The system uses Immediate Payment Service (IMPS) and Aadhaar Enabled Payment System (AEPS) for seamless money transfers.

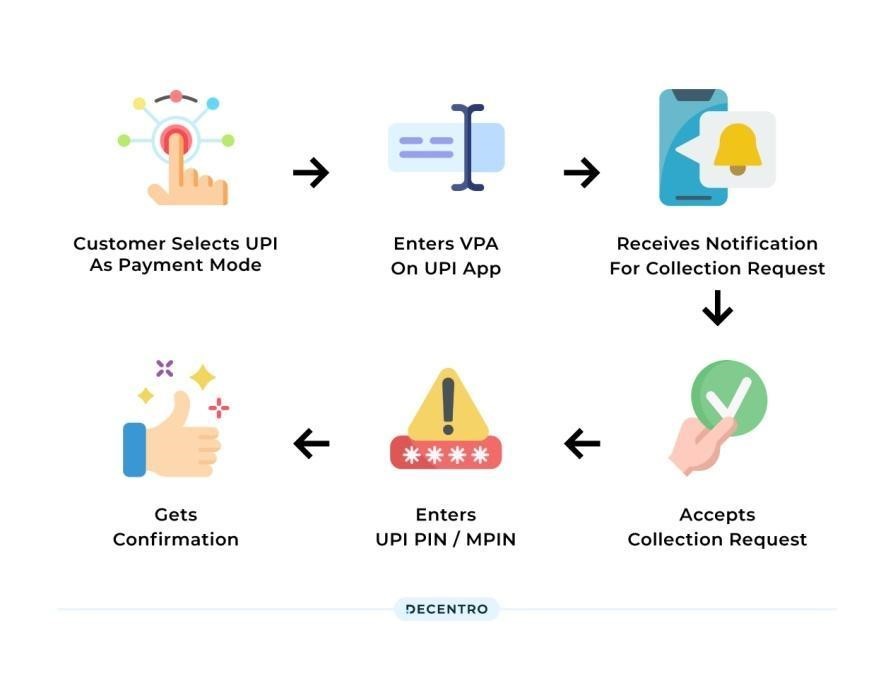

Working

- Setup – Download a UPI-enabled app (e.g., PhonePe, Google Pay, Paytm, BHIM), link your bank account, create a Virtual Payment Address (VPA) (e.g., name@bank), & set a UPI PIN for authentication.

- Transaction Flow – To send money, enter recipient’s UPI ID/scan QR, enter amount, confirm with UPI PIN.

- For request money, enter payer’s UPI ID, request amount, payer approves with UPI PIN.

- Both sender and receiver get instant confirmation.

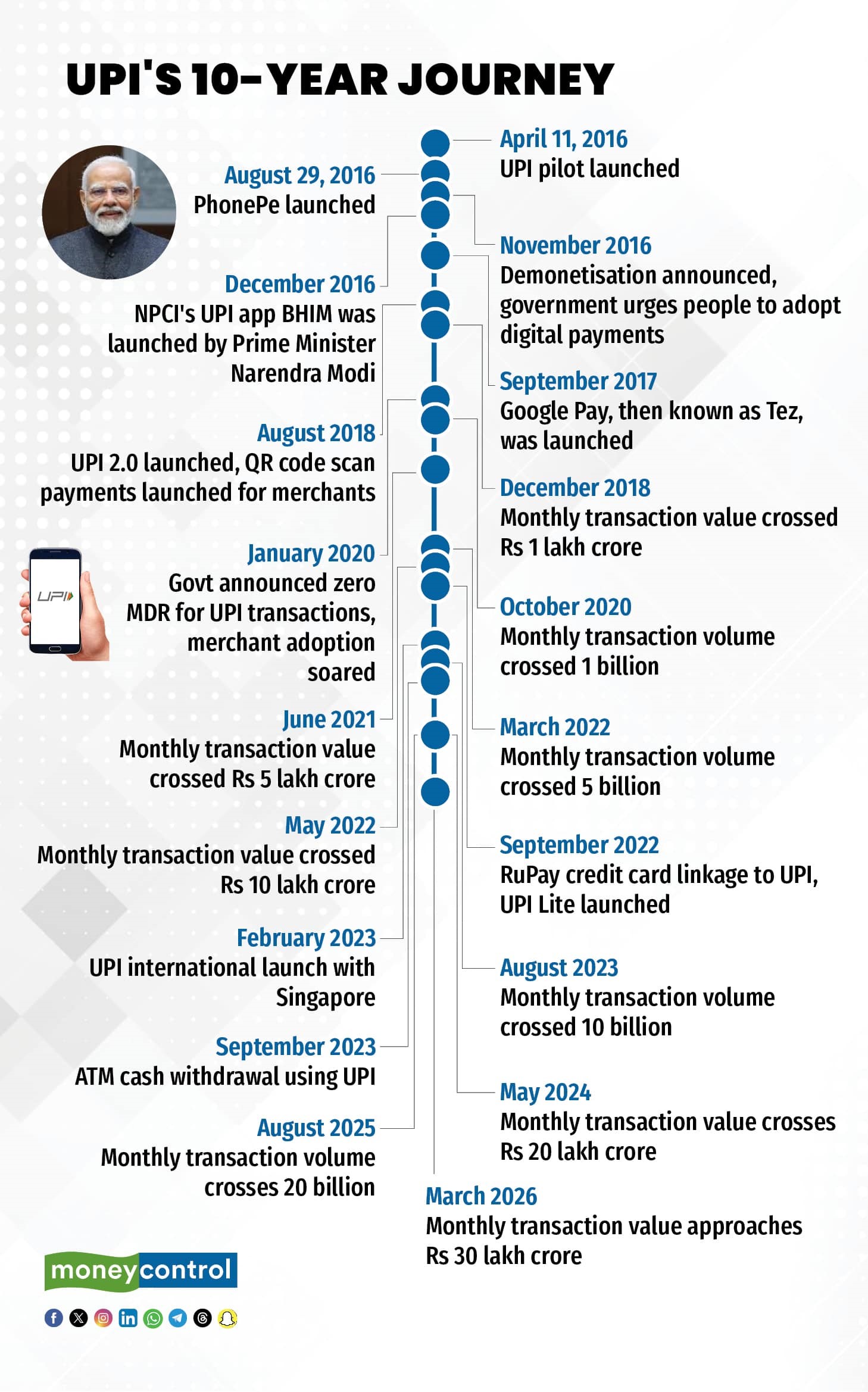

Journey of UPI

What is the present status of UPI in India?

- UPI’s Growth rate & Target – UPI is growing at a healthy rate of 30% and is now targeting a billion users over the next 10 years.

- User base – The platform currently has around 400 million active users.

- Nature of growth – The growth feels more organic now because the base is huge.

- But in absolute transaction volumes, expansion will remain relentless as UPI becomes a financial identity for all age groups and population segments.

- NPCI’s Innovation Drive with UPI – NPCI, which runs UPI, has kept up the pace of innovation even as the platform and the company have scaled up dramatically over the last 10 years.

- Ecosystem Scale – More than 700 banks plug into the UPI network.

- There are close to 50 third-party UPI apps (TPAP) like PhonePe and Google Pay.

- More than 100 financial apps connect to the network through partners.

- Smaller Players Rising – Navi, super.money, BHIM, WhatsApp Pay showing growth & new apps focusing on RuPay Credit on UPI: Kiwi, Jupiter, BharatPe, Scapia, all these could become major players in the next decade.

- Market Outlook – The pie is expanding, inevitably, no single player can serve all needs, will expect broad‑based players (general services) + specialists (recurring payments, credit products).

- Recent Launches

- Reserve Pay – AI‑powered agentic payments for e‑commerce without user intervention.

- Biometric Authentication – Fingerprint/face ID for UPI payments.

- UPI Circle – Delegated payments to others for minors & seniors with checks/controls.

- Credit Line on UPI (CLOU) – Access to micro‑credit.

- Hello UPI – Voice‑activated UPI payments.

- BillPay Connect – Facilitates chat-based bill payments.

- UPI Tap & Pay – Payments based on near-field communication (NFC) technology

- UPI Lite X – An on-device wallet facility.

- Cash Withdrawal in ATMs – via UPI without using cards.

- NPCI’s Strength and focus

- Infinite Scalability – UPI’s technology stack architecture allows for infinite scalability.

- It is designed for limitless growth, supporting massive transaction volumes.

- Reliability – UPI faces several failures at the bank-level, the system-wide outages are rare.

- NPCI has been working with banks to improve the technical decline (TD) rates (server unavailability issues) to reduce such incidents.

- From around 5-6% in 2020 and 2021, the TD rates have come down to below 1% for most large banks.

- Ownership & Model – NPCI is owned by the banks and other payment companies.

- Being a non-profit organisation, the organisation is likely investing all the profits to build more products and add more features.

What about the global impact created by the UPI?

- Focus on internationalization – NPCI is expanding UPI abroad and boosting RuPay credit cards with offers/partnerships.

- Global Recognition – India’s digital payments model praised by IMF and World Bank for scale, efficiency, inclusiveness.

- Leaders like Emmanuel Macron (President of France) highlighted UPI’s unmatched scale (over 20 billion monthly transactions).

- Cross‑border Expansion – UPI has expanded beyond India and is now linked with payment systems in

- UAE, Singapore, Bhutan, Nepal, Sri Lanka, France, Mauritius, and Qatar.

- Significance – This growing international footprint is facilitating cross-border transactions, supporting remittance flows, and contributing to financial inclusion, while strengthening India’s role in the global fintech landscape.

What are the concerns?

- Subsidies Declining – The central government subsidies for UPI have been declining since FY 24, even as transaction volumes keep rising.

- Fraud & Security Risks – Digital payment frauds are increasing & emerging tech like AI and quantum computing are likely to threaten security and strengthen defenses.

- Lack of monetisation – The payment companies have been requesting the government to implement the Merchant Discount Rate (MDR) on high value transactions or large merchants, who have an annual turnover of more than Rs 40 lakh.

- Merchant Discount Rate (MDR) – The fee businesses pay for digital transactions (like credit cards, debit cards, or UPI), it usually 1–3% of the transaction amount, covering bank and network processing costs.

- Credit Line on UPI (CLOU) offers some revenue, but scale is still too small.

- Infrastructure Strain – UPI processes 22 billion transactions/month or over 750 million transactions/day.

- It requires huge investment in data centers and robust tech stacks to handle peak loads.

- Ecosystem partners worry about long-term viability without stronger revenue streams.

- Two‑player dominance – PhonePe has around 45% market share followed by Google Pay at around 33% (together accounts for approximately 78%) & Paytm is 6%, much smaller share.

- The consumer market has sparked fears of systemic risks if any breach or outages happen at either of these companies.

- Several members of the Parliament has expressed fears of both these companies being owned by US-owned multinational firms, possible relief if PhonePe lists in India.

What are the future opportunities?

- Next phase of growth – The next focus is not just transaction value/volume, but bringing more people into the system.

- Credit Expansion – Enabled formal lending for underserved populations with a target of 500 million credit customers.

- Micro-credit – Provide micro-credit to the millions of underserved people in the country, who do not have access to formal credit at reasonable interest rates.

- Credit Line on UPI – It expected to become large and successful if more banks and non-banking financial companies could participate in the ecosystem.

References

- Money Control | UPI at 10: Next phase of growth

- Investopedia | UPI