Recently, National Payments Corporation of India (NPCI) has introduced interchange fees of up to 1.1% on merchant UPI transactions done using prepaid payment instruments.

|

Classification |

Description |

|

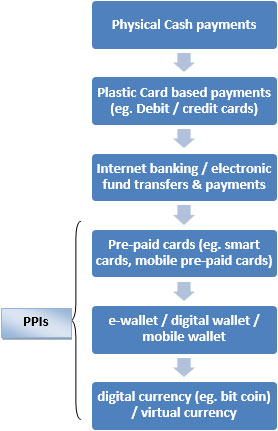

Closed System Payment Instruments |

|

|

Semi-Closed System Payment Instruments |

|

|

Semi-open System Payment Instruments |

|

|

Open System Payment Instruments |

|

Mobile Prepaid Instruments - The prepaid talk time issued by mobile service providers.

Interchange fee

A merchant discount rate, or MDR, is a rate charged to a merchant for the payment processing of debit and credit card transactions.

Quick facts

|

National Payments Corporation of India (NPCI) |

Initiatives of NPCI

|

References