Why in news?

Securities and Exchange Board of India (SEBI) has released a new framework for financial disclosure by credit rating agencies (CRAs).

What are credit rating agencies?

- Credit Rating Agencies (CRAs) are companies that evaluate the financial condition of issuers of debt instruments.

- CRAs assign a rating that reflects its assessment of the issuer's ability to make the debt payments.

- Rating is denoted by a simple alphanumeric symbol. E.g. AA+, A-, etc.

- In India, CRAs are regulated by SEBI (Credit Rating Agencies) Regulations, 1999 of the Securities and Exchange Board of India Act, 1992.

- The entities that are rated by credit rating agencies comprise companies, state governments, non-profit organisations, countries, securities, special purpose entities, and local governmental bodies.

- Some of the key CRAs in India include -

- Credit Rating Information Services of India Limited (CRISIL)

- ICRA Limited

- Credit Analysis and Research limited (CARE)

What are the new norms?

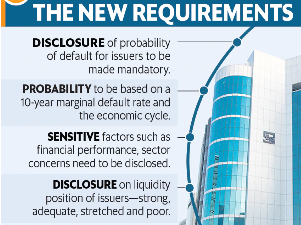

- Rating agencies have to clearly state the “probability of default” of the instruments they rate for the benefit of investors.

- Probability of default describes the likelihood of a default over a particular period.

- It provides the likelihood that a borrower will be unable to meet its debt obligations.

- SEBI will prepare and share standardised and uniform probability of default benchmarks.

- This will be fixed for each rating category for one-year, two-year and three-year cumulative default rates - both for the short run and long run.

- Probability will be based on a 10-year marginal default rate and the economic cycle.

- The agencies will also have to publish information on their performance in the rating of debt instruments, in comparison with a benchmark created in consultation with SEBI.

- This will help investors to better judge the performance of credit rating agencies.

- SEBI also introduced disclosure of factors to which the rating is sensitive.

- Rating agencies will have a specific section on rating sensitivities in each SEBI's press release.

- This would explain the broad level of operating and financial performance levels that could trigger a rating change - upward and downward.

- This is critical for the end-users to understand the factors that would have the potential to impact the credit worthiness of the entity.

- Besides, SEBI expects rating agencies to make meaningful disclosures on client’s liquidity position using simple terms.

- This may include terms such as superior or strong, adequate, stretched or poor.

- This should also come with appropriate explanations, to help the end users understand them better and avoid any ambiguity.

What is the rationale?

- The credibility of rating agencies has been eroding since the global financial crisis in 2008.

- This is primarily because of the conflict of interest arising from issuer-pays model.

- Under this, the ratings agency is paid by the issuer of the instrument that it rates.

- So agencies are found to be more loyal to companies whose instruments they rate rather than to investors who provide precious capital.

- CRAs as SEBI-registered intermediary are supposed to be an alert system of an instrument before the actual default.

- But after failing to detect early signs of the crisis, credibility of CRAs as an institution and their utility under the regulatory system were questioned.

- Given the impact of this over the larger economy, SEBI aimed at tightening the disclosure guideline.

- This is believed to enhance the quality of information made available to investors by the rating agencies.

- Overall, SEBI’s attempt seems to be to align ratings methodologies with global best practices.

- But it is not clear how the new framework will effectively resolve the conflict of interest issue that for long deteriorates the rating industry.

Source: The Hindu, Business Standard, Livemint