What is the issue?

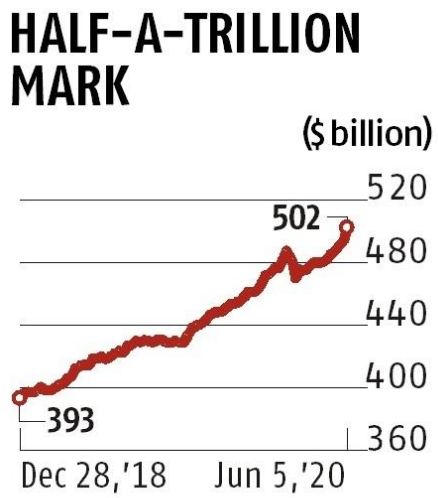

- India’s forex reserves crossed $500 billion for the first time ever in the week ended June 5, 2020.

- However, the nature of factors contributing to it and the economic uncertainties posed by the pandemic call for a cautious approach.

What are forex reserves?

- Forex reserves are external assets accumulated by India in the form of -

- gold

- SDRs (special drawing rights of the IMF)

- foreign currency assets (capital inflows to the capital markets, FDI and external commercial borrowings)

- These are controlled by the Reserve Bank of India.

Why is the present reserves position encouraging?

- The RBI was able to increase its reserves by $79 billion over the past year (FY19) and by $29 billion since the beginning of the 2020-21 fiscal year.

- The $500 billion mark comes as an encouraging development amidst the current gloomy economic scenario, given the COVID-19 pandemic.

- The reserves will be useful if global financial conditions deteriorate further, causing turbulence in currency markets.

What were the contributing factors?

- The dollar-rupee swap auctions conducted in March and April 2020 have helped increase reserves to some extent. [Click here to read on swap auction]

- But besides this, there is also a couple of other unplanned and some fortuitous developments as well.

- Notable among them are the rising external commercial borrowings (ECB) and an unexpected trade surplus.

- Global central banks are pumping in enormous amount of money into the global economy and moving interest rates lower.

- With this, Indian companies have found it easier to raise funds overseas at cheaper cost.

- Resultantly, ECBs raised in FY20 were 127% higher compared to FY19.

- In the first two months of 2020-21 fiscal, corporates had already borrowed over $2 billion.

What is the need for caution though?

- Increased overseas borrowing has downsides too.

- Corporates can struggle to roll over the loans if the rupee continues depreciating or if the interest rate cycle overseas turns adverse.

- It is also essential to be cautious about the favourable trade balance.

- This is because the current trade surplus is caused mainly by declining demand.

- Merchandise imports were sharply lower in April and May 2020, in line with contraction in global trade.

- Once domestic demand revives with the economy unlocking, demand for petroleum and other products is likely to revive.

- So, there might be pressure on the trade balance once again.

- On the other hand, foreign portfolio investments have not been too robust in 2020.

- FPIs (Foreign Portfolio Investors) have turned net buyers in equities in May and June 2020.

- However, they could turn net-sellers again if risk-aversion spikes.

- That might cause outflows from global emerging markets, if the pandemic does not settle down by the end of this year.

- Likewise, foreign direct inflows were strong until March 2020.

- Inflows in FY20 were 40% higher compared to the previous fiscal year.

- But, direct investments are likely to be much lower in FY21 as businesses struggle to stay afloat amidst the pandemic.

- Remittances from NRIs are also likely to be lower with many overseas Indians witnessing pay-cuts or job losses.

How does the future look?

- Given the above uncertainties, the RBI is being only prudent in its strategy to continue buying dollars.

- This adds to the buffer as well as helps to keep the rupee weak, making it competitive in the export market in relation to its peers.

- [Notably, the Indian currency is down 4.5% so far in 2020.]

- Other countries have also witnessed an increase in their forex reserves in the May and June 2020.

- This highlights the fact that India needs to be ready to face future turbulence.

Source: BusinessLine