Why in news?

The Ministry of Statistics and Programme Implementation (MoSPI) has released the data for -

- the 4th quarter (January to March) of the last financial year (2019-20)

- the provisional estimates of the full-year GDP growth rate

What is the GDP growth projection?

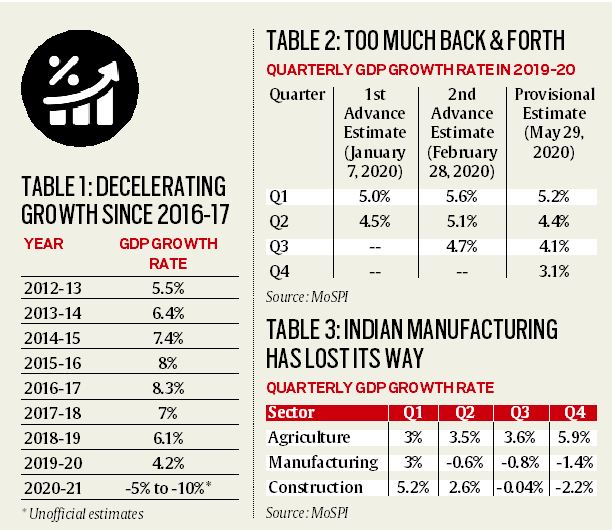

- The data report states that the Indian economy grew by 4.2% in 2019-20.

- This is the lowest annual growth rate of GDP registered under the new GDP data series with base year 2011-12.

- In contrast, the government had expected in July 2019 when it presented the Budget for that year a growth of 8.5%.

- It is also significantly lower than the 5% that the Second Advance Estimates suggested at the end of February 2020.

What is the nominal GDP scenario?

- The above is the growth rate in real GDP.

- A similar fall can be seen in the trajectory of the nominal GDP as well.

- [Real GDP is arrived at by subtracting the nominal GDP growth by the inflation level.]

- At the time of the 2019-20 Budget presentation in July 2019, nominal GDP was expected to grow by 12%-12.5%.

- The provisional estimates peg it at just 7.2%. [In 2018-19, the nominal GDP grew by 11%.]

- The sharp deceleration in nominal GDP growth, more than anything else, shows the continued weakening of India’s growth momentum.

- This was the case even before the economy was hit by the Covid-19 induced lockdown.

Why is this a big concern?

- First of all, the nominal GDP growth rate is the base of all fiscal calculations in the country.

- The government bases its calculations on this initial assumption.

- E.g. the amount of revenues the government will raise and the amount of money it will be able to spend

- A sharp fall in nominal GDP growth rate means the government does not get the revenues it had hoped for and, it cannot spend as much as it wanted to.

- Secondly, the substantial deceleration in nominal GDP growth reflects poorly on the government’s fiscal prudence.

- In other words, it shows that the government was not able to assess the magnitude of economic growth deceleration that was underway.

- Government's poor fiscal marksmanship, in turn, leads to inaccurate policy making.

- This is because a government could end up making policies for an economy that does not actually exist on the ground.

- E.g. in an economy that was slowing down sharply and that too on account of a demand decline, even a massive corporate tax cut would be ineffective

- Certainly, despite this once-in-a-generation reform (tax cut), private investments actually fell by almost 3% in 2019-20.

- This remains in sharp contrast to the 9% increase in 2018-19.

What is the concern with frequent revisions in quarterly GDP?

- India’s national income accounting data (the new GDP data series with base year 2011-12) has been under criticism in the past.

- Arvind Subramanian (2014-2018 Chief Economic Advisor to Finance Ministry) argued, in 2019, that the new series overestimated India’s GDP by as much as 2.5 percentage points.

- While that debate remains unsettled, the credibility of India’s GDP estimates is weakened by frequent and significant revisions.

- The provisional estimates have fluctuated repeatedly.

- E.g. the growth estimate for Q2 (July, August and September) has gone from 4.5% to 5.1% and back to 4.4% in just 5 months (between January and May 2020)

- In essence, it is now becoming clear that all through 2019-20 India’s growth rate was decelerating much faster than what was officially accepted at that time.

What is the larger concern?

- Another key takeaway from the provisional GDP estimates is the undesirable emerging structure of the Indian economy.

- It has been widely argued, that for India to grow and create jobs for the millions that enter its workforce each year, manufacturing growth has to rise.

- Together with services, manufacturing growth was supposed to absorb the millions still dependent on agriculture.

- [Agriculture, even when it grows fast, does not have the ability to raise per capita income in a big way.]

- If India was to create lots of well-paying jobs that allow it to reap the so-called demographic dividend then it had to be via manufacturing growth.

- But 2019 figures in manufacturing are less encouraging.

- While the agriculture and allied sectors enjoyed buoyant growth, as the year progressed, manufacturing simply lost its way.

- The growth in this sector contracted for three of the four quarters of the year.

What does all this mean?

- The estimates for 2019-20 just support the notion that the growth deceleration since 2016-17 simply became worse as the last financial year progressed.

- In the last quarter of the financial year, the economy grew by just 3.1%.

- It shows that the economy had already become quite vulnerable before Covid-19 hit India at the end of March 2020.

- Prospective intervention is essential to alter the course.

Source: Indian Express