Why in news?

Recent data from the Central Statistical Office (CSO) indicates a slowdown in industrial growth and an increase in inflation numbers.

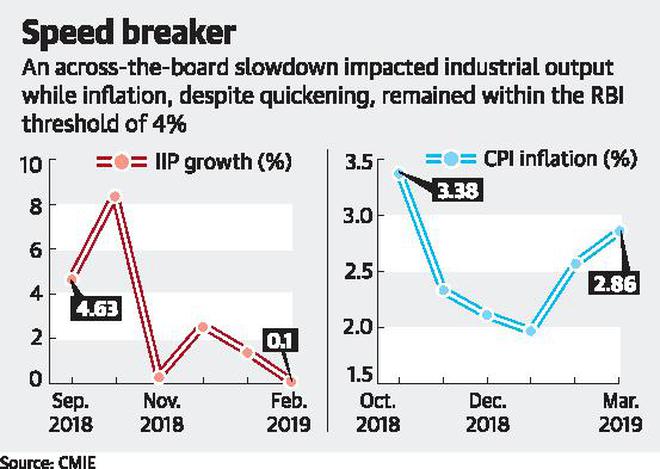

How is the industrial growth?

- Growth in the Index of Industrial Production (IIP) slowed in February, 2019 to 0.1% (a 20-month low) from 1.44% in January.

- An across-the-board slowdown, especially in key sectors like manufacturing, mining, capital goods, and infrastructure has driven this.

- Within the Index, the mining and quarrying sector saw growth slowing to 2% from 3.92% over the same period.

- The manufacturing sector (with a weight of almost 78% in the index) saw a contraction of 0.31% in February from 1.05% in January.

- The largest contributor to the slowdown in February was the capital goods sector.

- The sector continued its contraction in February by 8.84% compared with a contraction of 3.42% in the previous month.

- Growth in the infrastructure sector slowed to 2.38% from 6.8%.

- The electricity sector was the only sector that saw an acceleration in growth; 1.18% in February compared with a growth of 0.94% earlier.

- The consumer non-durables sector also saw growth quickening, to 4.3% from 3.33% over the same period.

What is the inflation scenario?

- Retail inflation, as measured by the consumer price index (CPI), has gone up in March, 2019 to a five-month high.

- It has increased to 2.86% in March, 2019 from 2.57% in February.

- It was largely driven by the speeding up of inflation in the food and fuel sectors.

- Inflation in the food and beverages segment of the CPI quickened to 0.66% in March compared with a contraction of 0.07% in February.

- Inflation levels in all the other segments of the CPI came in lower, however.

- So overall inflation is still well below the average threshold of 4%.

How is the overall economic scenario?

- GDP grew by just 6.6% in the quarter ended December, the slowest pace in six quarters.

- Other economic indicators such as the purchasing managers’ index and automobile sales are also signalling weakening momentum. Click here to know more.

- So the overall scenario, when viewed along with industrial output slowdown, suggests that a turnaround in economic growth is not in sight.

- Various institutions such as the RBI and the International Monetary Fund have been lowering their expectations for India’s growth in the coming quarters.

What is to be done?

- The downturn in industrial activity and the spike in retail inflation clearly pose a policy challenge.

- On the fiscal side, the prospects are limited as both direct and indirect tax revenue collections have shown a shortfall compared to the revised estimates.

- But to meet the 3.4% fiscal deficit target, the government seems to be curtailing expenditure in general, and capital expenditure in specific, which is not a healthy trend.

- So the outlook should be thought of in terms of stimulating investment demand in the economy.

- On the monetary side, steps have been taken through two successive rate cuts by the Reserve Bank of India.

- But beyond this, policymakers should also look into the structural issues behind the slowdown.

- The high levels of troubled debt in not just the banking sector but the wider non-banking financial companies are hurting credit markets.

- Notably, to a large extent, the slowdown is due to weakening investments as the credit cycle tightened.

- Easing interest rates without reforms may only help hide investment mistakes instead of fostering a genuine economic recovery.

- So addressing the structural issues is essential to fully reap the benefits of any rate cuts by the RBI and make an effective stimulus.

Source: The Hindu

Author: Shankar IAS Academy Trichy

Visit for Daily Current Affairs on Indian Economy